Credit card interest rate margins at all-time high

By some measures, credit cards have never been this expensive. For cardholders who carry a balance without paying it off in full each month, issuers generally charge interest based on annual percentage rates (APRs). In 2022 alone, major credit card companies charged over $105 billion in interest, the primary cost of credit cards to consumers. While the effects of increases to the target federal funds rate have received considerable attention, the average APR margin (the difference between the average APR and the prime rate) has reached an all-time high.

In this analysis, we show that higher APR margin drove about half of the increase in credit card rates over the last decade. In 2023, excess APR margin may have cost the average cardholder over $250. Major credit card companies earned an estimated $25 billion in additional interest revenue by raising APR margin. Increases to the average APR margin - despite lower charge-off rates and a relatively stable share of subprime borrowers - have fueled issuers’ profitability for the past decade. Higher APR margins have allowed credit card companies to generate returns that are significantly higher than other bank activities.

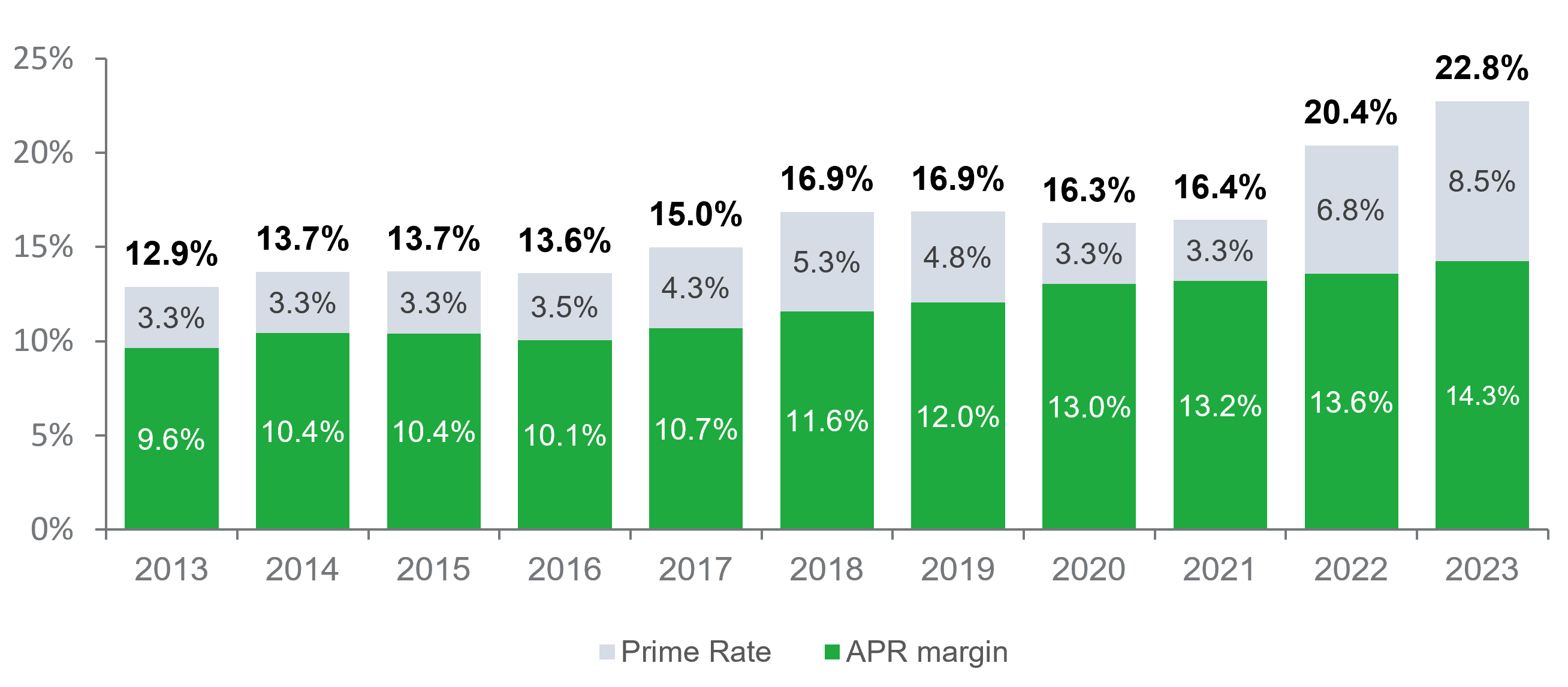

Credit card average APR margin is the highest on record.

Over the last 10 years, average APR on credit cards assessed interest have almost doubled from 12.9 percent in late 2013 to 22.8 percent in 2023 — the highest level recorded since the Federal Reserve began collecting this data in 1994. The APR on most credit card accounts can be viewed as being composed of the prime rate and the APR margin. The prime rate (a benchmark most banks use to set rates) represents a good proxy for banks’ funding costs, which have increased in recent years. But credit card issuers have also sharply increased average APRs beyond changes in the prime rate.

Nearly half of the increase in average APR over the last 10 years has been driven by issuers raising their APR margin. APR margin for revolving accounts is now at 14.3 percent, the highest point in recent history. More than half of issuers sent offers by direct mail with a higher APR margin in the third quarter of 2023 than on the same product the year before, according to our analysis of Competiscan data.

Figure 1: Average APRs on Accounts Assessed Interest and Average Prime Rate at Year End

Source: Federal Reserve

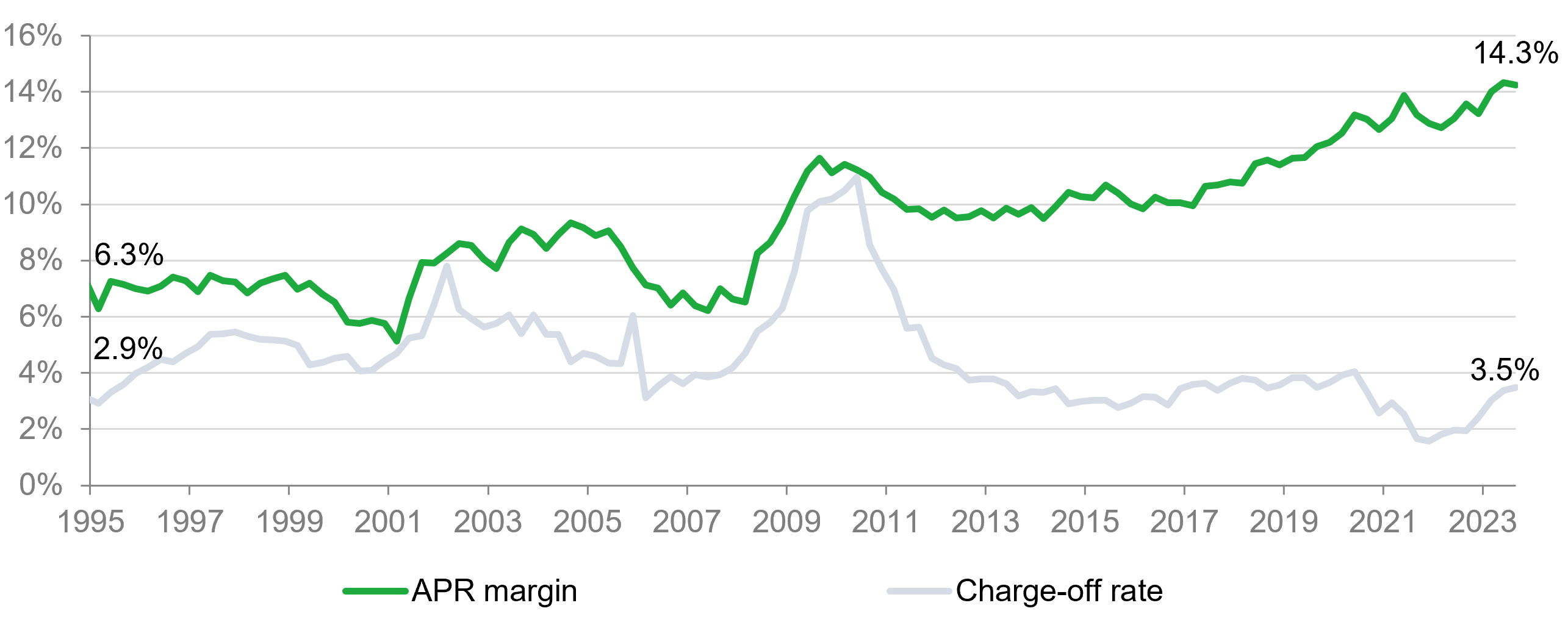

Higher APR margin has fueled the profitability of revolving balances.

Typically, card issuers set an APR margin to generate a profit that is at least commensurate with the risk of lending money to consumers. In the eight years after the Great Recession, the average APR margin stayed around 10 percent, as issuers adapted to reforms in the Credit Card Accountability Responsibility and Disclosure Act of 2009 (CARD Act) that restricted harmful back-end and hidden pricing practices. But issuers began to gradually increase APR margin in 2016. The trend accelerated in 2018, and it continued through the pandemic.

Over the past decade, card issuers increased APR margin despite lower charge-off rates and a relatively stable share of cardholders with subprime credit scores. The average APR margin increased 4.3 percentage points from 2013 to 2023 (while the prime rate was nearly 5 percentage points higher). As such, the profitability of revolving balances excluding loan loss provisions (the money that banks set aside for expected charge-offs) has been increasing over this time period.

Figure 2: Average APR Margin and Charge-Off Rate (Federal Reserve)

Source: Federal Reserve

Excess APR margin costs consumers billions of dollars a year.

In 2023, major credit card issuers, with around $590 billion in revolving balances, charged an estimated $25 billion in additional interest fees by raising the average APR margin by 4.3 percentage points over the last ten years. For an average consumer with a $5,300 balance across credit cards, the excess APR margin cost them over $250 in 2023. Since finance charges are typically part of the minimum amount due, this additional interest burden may push consumers into persistent debt, accruing more in interest and fees than they pay towards the principal each year — or even delinquency.

The increase in APR margin has occurred across all credit tiers. Even consumers with the highest credit scores are incurring higher costs. The average APR margin for accounts with credit scores at 800 or above grew 1.6 percentage points from 2015 to 2022 without a corresponding increase in late payments.

Credit card interest rates are a core driver of profits.

Credit card issuers are reliant on revenue from interest charged to borrowers who revolve on their balances to drive overall profits, as reflected in increasing APR margins. The return on assets on general purpose cards, one measure of profitability, was higher in 2022 (at 5.9 percent) than in 2019 (at 4.5 percent), and far greater than the returns banks received on other lines of business. Even when excluding the impact of loan loss provisions, the profitability of credit cards has been increasing.

CFPB research has found high levels of concentration in the consumer credit card market and evidence of practices that inhibit consumers’ ability to find alternatives to expensive credit card products. These practices may help explain why credit card issuers have been able to prop up high interest rates to fuel profits. Our recent research has shown that while the top credit card companies dominate the market, smaller issuers many times offer credit cards with significantly lower APRs. The CFPB will continue to take steps to ensure that the consumer credit card market is fair, competitive, and transparent and to help consumers avoid debt spirals that can be difficult to escape.