High Interest Rates Set to Increase the Cost of Student Loans in 2024

Higher student loan interest rates could cost students over $3 billion in additional interest for loans taken out in this year alone

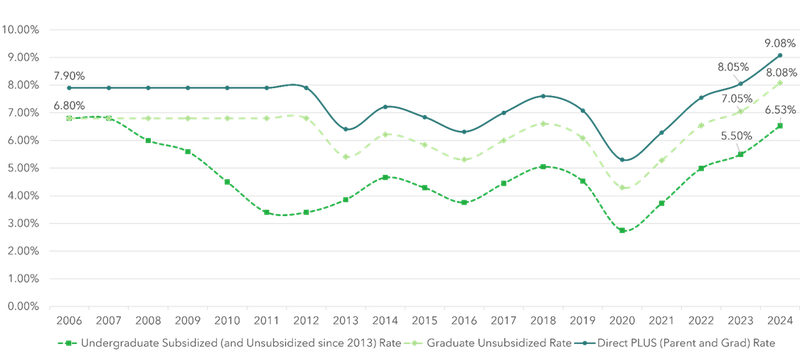

On July 1, interest rates for new federal student loans rose to their highest levels since before the Great Recession. Interest rates for undergraduate loans have increased to 6.53% this year, nearly a 19% increase over last year and a 44% increase from just five years ago. For graduate and parent borrowers, costs were raised to their highest levels since 2006, with interest rates set over 9% (Figure 1). These higher interest rates could cost students over $3 billion in additional interest for loans taken out in this year alone.1

Figure 1: Federal Student Loan Interest Rates, 2006 - 2024

Borrowers Will Pay Substantially More

Increasing student loan interest rates will cost borrowers thousands of dollars. For example, for an undergraduate student leaving school in 2025, a student loan for the final year of college will cost $466 more compared to the same loan taken out just one year ago. For a graduate student or parent borrower, their final year of student loans will cost $497 more (Figure 2). And these additional costs are for only one year of borrowing, so the true cost of the increased rates could be much higher. Although student loan borrowers may be able to lower monthly payments through income-driven repayment plans, interest continues to accrue under most plans, and borrowers may be unaware of these repayment plans , have difficulty accessing them or, in some cases, may still struggle to make ends meet despite the availability of these options.

Figure 2: Difference in Repayment Amounts for a $7,500 Student Loan Taken Out in 2024-2025 Compared to the Prior Year2

| Repayment Plan | Difference in Lifetime Repayment (Undergrad) | Difference in Lifetime Repayment (Graduate) | Difference in Lifetime Repayment (Parent PLUS) |

|---|---|---|---|

Standard Repayment |

$466 |

$485 |

$497 |

Graduated Repayment |

$615 |

$655 |

$576 |

SAVE Plan |

$0 |

$0 |

Ineligible |

Borrowers Have Few Good Options When Rates Rise

Federal student loans are unusual compared to many private credit products because interest rates are fixed by a formula defined by Congress. Even if interest rates decrease for future student loan originations, the rate on federal student loans remains the same throughout the repayment period. As a result, borrowers who take on federal student loans this year will always make higher payments than others who borrow in a lower interest rate environment.

This leaves borrowers caught between two choices: (1) a lower rate through private loans which could help them afford everyday essentials, but cost them the important protections that come with federal student loans, or (2) a loan with a higher rate that comes with the protections of a federal student loan.

The CFPB is also aware that private lenders may overstate the savings and benefits of their products. We recently observed instances where private student loan servicers improperly denied benefits to eligible borrowers and failed to honor legal protections afforded to all borrowers by law. Additionally, borrowers frequently report problems they have with private student loans to the CFPB, such as improperly assessed fees, improperly denied deferment requests, frustration with ballooning balances, and misleading information during the origination and refinancing processes.

The CFPB will continue to examine the effect interest rates have on borrowers, and it will ensure that student loan companies comply with federal consumer financial protection laws.